In addition to our quarterly reports on the new, resale and rental condominium apartment markets, Urbanation is actively engaged in site-specific market studies across the country. Interestingly, the majority of our consulting work has been focused on the market opportunity to construct new purpose-built rentals.

Whether it’s the fact that rental demand is at a 25-year high (at least), that condo rents have grown by about 20% over the past five years, that vacancy rates are ultra-low, the availability of low interest loans and tax incentives to build new rentals, or the perhaps the diversification of developers away from condos, attention has shifted sharply to the purpose-built arena.

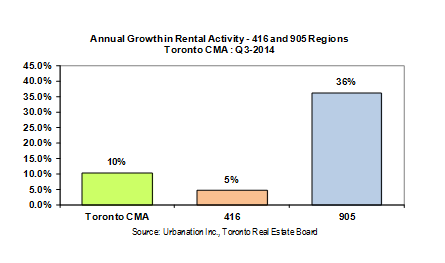

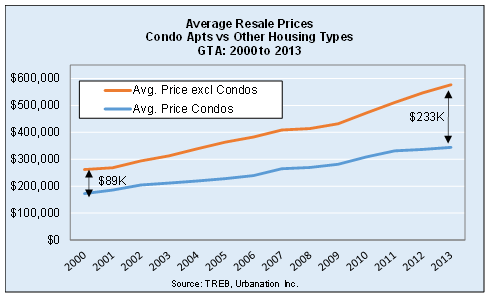

With condos representing 99% of new rental supply in the GTA, our ability to provide accurate market valuation assessments has benefited tremendously by drawing information from the UrbanRental database — our proprietary database of condo rental market data by project.

In the course of conducting our research we have come across several instances where new purpose-built projects have been achieving higher per sq. ft. rents than comparable condo projects. For this blog post, we decided to zero in on some examples within the City of Toronto.

Five recently completed rental apartments were selected: One32 (2013), Motion (2012), WestQ (2012), Minto Roehampton (2007), and Jazz (2006). Using the UrbanRental database, we identified condo projects that were (i) within a 500 metre radius of the site, (ii) built within the last 10 years, and (iii) were of a comparable scale as the rental buildings selected.

One obvious impediment in making rent comparisons between purpose-built and condo projects was the difference in sample size — condo transactions were plentiful in the year-to-date 2014 while rental information for purpose-builds was relatively scare due to low unit availabilities. The data used to represent rental projects for this study were obtained via their websites or through the property management offices.

The map below shows the location of the purpose-built rental projects examined represented by blue markers and their surrounding comparable condos by red markers.

Four out of the five purpose-built projects surveyed had higher per sq. ft. rents than their surrounding condo projects. Within the four projects, premiums ranged from 1.4% or $0.04 psf (Jazz) to 7.2% or $0.20 psf (Minto Roehampton). Differences in unit sizes played some part in the purpose-built premium (smaller units tend to generate higher psf rents), with suites at Minto Roehampton roughly 130 sf smaller than leased condos in the area. Slight variations in location, buildings age, suite layouts and finishes, project amenities, and floor heights of the units surveyed may also explain some of the gap. However, across the four projects these differences appear to mostly balance out and the average premium for purpose-built units was 4.4% or $0.12 psf.

When including Motion, which posted lower psf rents than its condo comparables (mostly due to having a larger range of suite sizes), the average premium across the five projects falls to 1.7% or $0.05 psf.

In the end, the results indicate that there does appear to be at least some premium achieved by purpose-built rentals over competing condo supply. All else being equal, renters tend to favour a professionally managed and secure source of housing. Of course values in new purpose-built projects can also receive a boost due to their scarcity.

The findings are encouraging for rental operators who will continue to face competition from a high volume of investor-owned condos coming to completion in the next few years. However, beyond 2017, condo supply growth will slow considerably due to fewer project launches over the past two years. This further supports the case for considering purpose-built development today.

For more information on this research or to inquire about Urbanation’s UrbanRental reports and consulting services, please contact Shaun Hildebrand at (416) 922-2200 or shaun@urbanation.ca

{kind=link}